Despite the expanding role satellite providers have in delivering connectivity, the vast majority of intercontinental capacity is carried by submarine cables.

This will likely always be the case, but new constellation projects are poised to reshape how broadband is delivered to end users.

For years, both large corporations and startups alike have shown interest in deploying satellites for broadband. This interest is mostly—but not entirely—rooted in bringing less-connected markets to the global internet. We’ve even explored if this means satellite traffic could overtake submarine cables (spoiler: it does not).

But what does the rise in satellite investment mean for broadband prices?

A Satellite Resurgence

First, let’s remind ourselves of how the satellite market has evolved until now.

Some of the earliest satellites used for telecommunications fly in what is called geosynchronous equatorial orbit (GEO). These circle the earth from a far distance maintaining roughly the same position above the surface of the planet.

Most planned satellite constellations used for connectivity fly in low earth orbit (LEO). These tend to have lower latency and higher bandwidth than their GEO counterparts.

Despite the advantages of LEO satellites, the high cost of development and launching has been a barrier for some time. And because they fly lower than GEO satellites, covering less terrain, there need to be more LEO satellites for global coverage. Plus LEO satellites wear out quickly, meaning they need to be replaced every five years or so.

What’s New and Who’s Who?

Where does that leave us in today’s market?

Connectivity by satellite in its present state is mostly a last resort. Think of in-flight aircraft sessions, cruise ships, users on remote islands and mountain trails, and other geographically isolated scenarios such as oil rigs and agricultural fields as examples.

There are presently a few main companies with potential to alter the landscape via LEO satellite broadband: SpaceX (through Starlink), Amazon (Project Kuiper), OneWeb, and the State Grid Corporation of China.

While many others have similar satellite ambitions, these four currently plan to launch the most units into space. The European Union has also announced plans to initiate space-based connectivity by 2024, but hasn’t specified their expected constellation size.

As of their March 2021 launch, Starlink alone has over 1,300 active satellites. And they currently have permission to increase that number up to at least 4,408, with the long-term goal of having roughly 42,000 satellites in orbit.

As of their March 2021 launch, Starlink alone has over 1,300 active satellites. And they currently have permission to increase that number up to at least 4,408, with the long-term goal of having roughly 42,000 satellites in orbit.

To add some context, there are roughly 3,000 satellites in operation today. About 2,000 of those are LEO satellites.

Of the projects mentioned above, Starlink already has active constellations serving beta broadband customers.

A Failure to Launch

Much of the internet-by-satellite market to date has been hard to sustain.

Some companies like O3b (now owned by SES) and Google’s now-defunct broadband-by-balloon Project Loon have focused on connecting the unconnected to the global economy. Notably, neither of these examples works in low earth orbit.

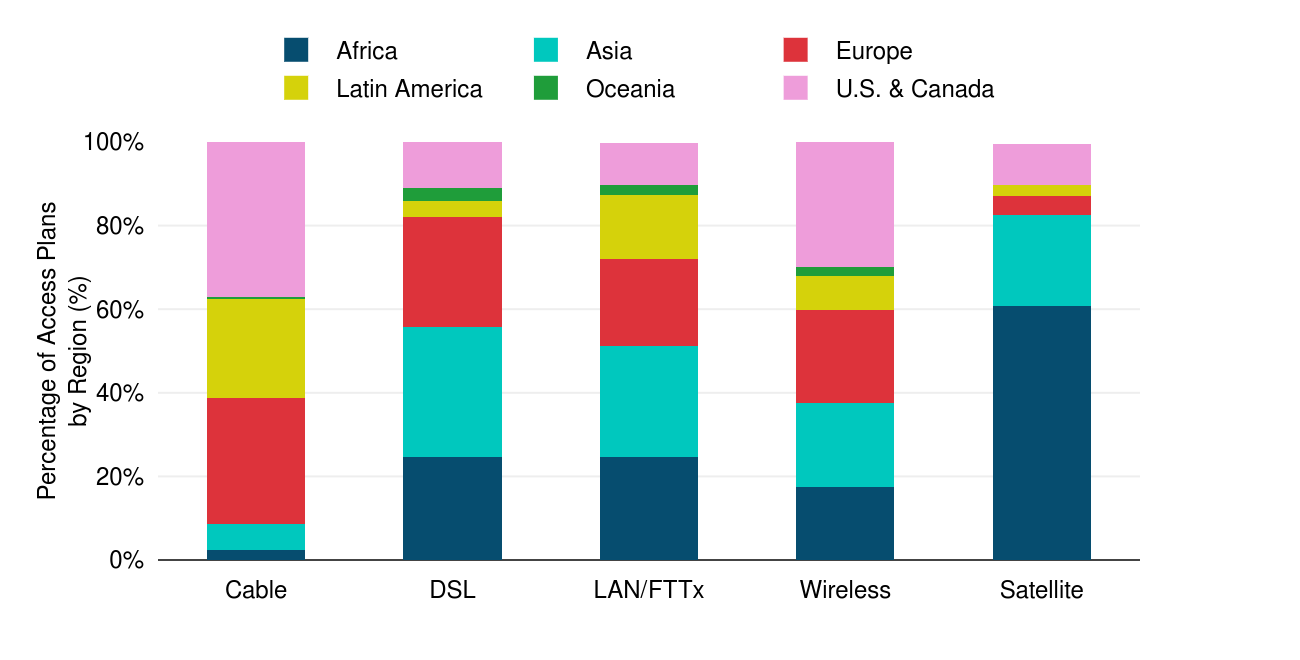

Some of the larger broadband satellite predecessors to Starlink and Amazon’s Kuiper are Telesat, Viasat, Hughes, Intelsat, and SES. Globally, satellite broadband tends to serve regions with more connectivity barriers. The figure below from our business broadband research shows Africa and Asia make up the vast majority of satellite business broadband use.

Recovering the Satellites

Access Plans by Region

Starlink, Kuiper, and OneWeb might be best positioned to target unconnected customers in under-connected markets. This means people who live where networks exist, but who lack connectivity from their specific locations. Think rural Oregon or peripheral neighborhoods in Buenos Aires rather than the Congo or Siberia.

Those aspiring to provide broadband to unconnected locales will likely face high costs as a continual barrier. Some of this can be alleviated by government subsidies, but these are often not available uniformly.

Those aspiring to provide broadband to unconnected locales will likely face high costs as a continual barrier. Some of this can be alleviated by government subsidies, but these are often not available uniformly. For example, SpaceX received $886m for Starlink from the U.S. Federal Communications Commission. Similar investment in smaller economies will be harder to acquire.

How Could LEO Broadband Impact Prices?

So to address the multi-million dollar question: how might more satellites affect broadband prices for end users?

At its core, this is a question of market competition. The arrival of Starlink and others could diversify broadband competition in some places by shifting a market with one or two carriers to having two or three options. Or even zero to one.

During its current “Better than Nothing” beta release, Starlink has indicated prices at $99/month on top of a one-time $499 equipment fee, with download speeds getting up to 100 Mbps or higher.

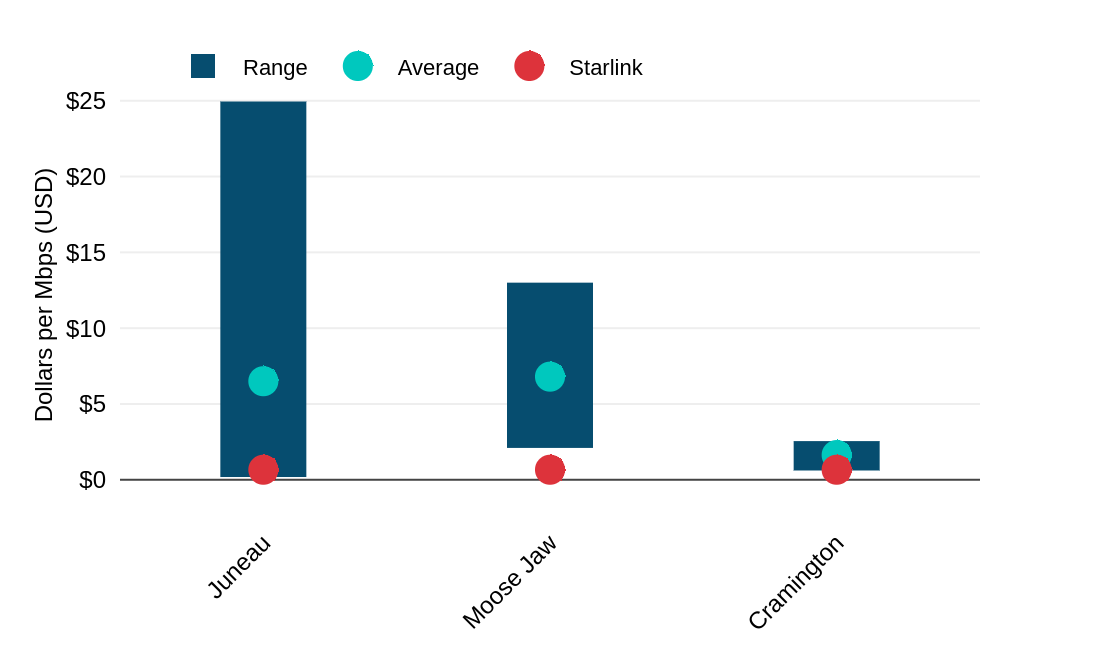

If we compare this to available broadband options at northern latitudes in countries where Starlink plans to launch initially we see that the cost per Mbps compares favorably to other plans and falls on the low end. If Starlink’s speeds double to 300 Mbps, as SpaceX CEO Elon Musk has suggested, this rate will drop further.

Hitch Your Wagon to a Star

Northern Latitude Broadband Prices in Starlink Countries

We know that when new competition enters a market the prices tend to drop. So if Starlink or any other broadband provider can maintain a presence in an expensive area, that could lead to lower prices across the board.

However, a sudden price drop due to Starlink seems unlikely, at least on a global scale.

Simply sending satellites into space is only part of the equation. To actually create new broadband connections, those satellites need to connect with ground stations that feed into subsea and terrestrial networks.

Considering the costs of erecting hundreds (or potentially thousands) of new ground stations, there is reason to believe Starlink won’t suddenly revolutionize previously unconnected regions. But it could be the catalyst to satellite broadband market growth.

Peter Wood

Peter Wood is a Senior Research Analyst at TeleGeography. His work is focused on network services and pricing with a regional focus on Latin America and the Caribbean.