Now that internet backbone operators have adapted their networks to accommodate changes in traffic flows, they've resumed a more measured approach to capacity planning and network upgrades in 2021.

That means that price trends have resumed their downward trajectory and regional characteristics accordingly.

Across a range of markets, 10 GigE prices fell 18% compounded annually from Q2 2018 to Q2 2021. A comparable sample of 100 GigE port prices fell 30% over the same period.

What's the takeaway? Well, the sharper decline in 100 GigE reflects the advanced maturity of 10 GigE.

While 10 GigE remains a relevant increment of IP transit—particularly in emerging markets—its share of the transaction mix continues to yield to 100 GigE. Most internet backbone operators have 100 GigE deployed, many with multi-100 GigE transactions.

While 10 GigE remains a relevant increment of IP transit—particularly in emerging markets—its share of the transaction mix continues to yield to 100 GigE. Most internet backbone operators have 100 GigE deployed, many with multi-100 GigE transactions.

Following early speculation that the next increment of port capacity might jump to 1 Tbps, operators are poised to adopt 400 GigE IP transit ports as the next fundamental upgrade from multiple 100 GigE ports.

Customers with the highest traffic commitments receive the best price.

IP transit transactions—which are expressed as unit price per Mbps—are lowest for full port allocation. In Q2 2021, the lowest 10 GigE prices on offer were at the brink of $0.09 per Mbps per month. The lowest for 100 GigE were $0.06 per Mbps per month.

On the Way Down

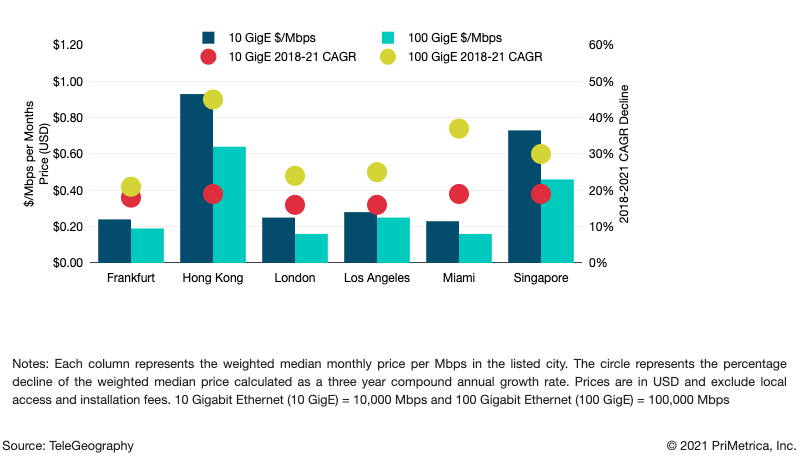

Weighted Median 10 GigE and 100 GigE IP Transit Prices & Three Year CAGR Decline in Major Global Hub Cities

Price erosion for 100 GigE ports in the cities above has exceeded that which we've noted for 10 GigE ports significantly: 30% versus 18%. Simply put, this is attributed to more carriers offering it and more competition.

On average, across the cities noted, the monthly recurring charge for a 100 GigE port is just over seven times the MRC for a 10 GigE port.

A Bigger Picture

IP transit providers achieve competitiveness with network scale and traffic volumes. Continued investment in international infrastructure delivers capacity at the lowest unit cost and creates opportunities to aggregate traffic and sell IP transit outside the major hubs.

Recent price declines have been greatest in emerging markets where prices are relatively high—particularly in Latin America.

Emerging markets have the greatest potential for improvements in volume growth and local or regional traffic exchange. Markets with improving economies of scale have the greatest potential for price erosion, while markets lacking these improvements harbor higher prices.

In established global hubs, prices continue to fall, driven by the most advanced network economics.

More and more, backbone providers are selling 100 GigE ports rather than 10 GigE ports. They're deploying 400 GigE ports and looking forward to transit transactions with that infrastructure. Increasing volume will only decrease the cost of the ports, perpetuating the cycle of shrinking unit cost and price.

In our Global Internet Geography research service, we discuss the impact of COVID-19 within the larger framework of our analysis and statistics on internet capacity and traffic. We also discuss factors impacting IP transit pricing and the role individual backbone operators play. This content comes from our latest report update.

To become a Global Internet Geography subscriber, email us at sales@telegeography.com.

Nataliya Coll

Nataliya Coll is a Senior Research Analyst at TeleGeography. As part of the pricing team, she contributes wholesale and enterprise product analysis. Nataliya focuses on European and Eurasia markets.