It is said that only three things are certain in life. The future of the global bandwidth market is not one of them.

Beyond persistent demand growth and price erosion—the two most predictable trends—operators will have to navigate the major uncertainties of an evolving sector.

According to our freshly updated Global Bandwidth Research Service, these key factors will impact the long-haul capacity market in the coming years.

Rising Utilization

The most fundamental driver for new cable construction is the limited availability of potential capacity.

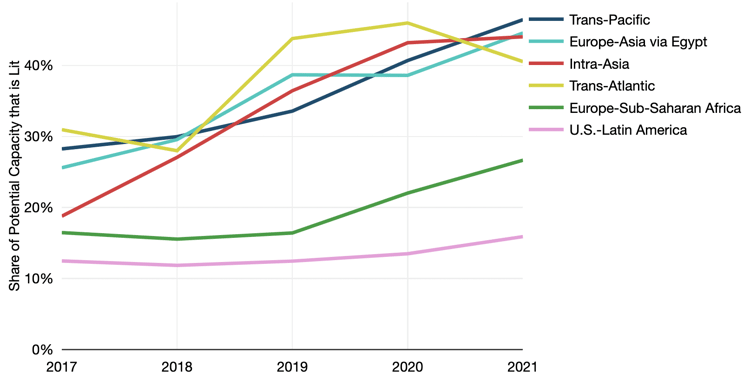

On the surface, this issue may not appear important on major cable routes, where the percentage of potential capacity that is lit has only recently exceeded 30%.

Even with the introduction of many new cables and the ability for older cables to accommodate more capacity, the growth of potential capacity has failed to outpace that of lit capacity. As you can see in the figure below, this means that the share of capacity that is lit on major routes has begun to rise.

Percentage of Potential Capacity that is Lit on Major Submarine Cable Routes

Looking at the lit share of potential capacity is not the only way to measure utilization.

In fact, the availability of fiber pairs is emerging as a key metric on routes where content providers are involved. Thus, when gauging potential supply on a route, it's important to bear in mind not just how much unlit capacity remains, but whether unlit fiber pairs are available as well.

Uncertain Growth for Content Providers

Content providers' international capacity has grown at a rapid rate in recent years, but how long can this last?

Most network planners in these companies focus on meeting expected growth for a 2- to 3-year planning horizon. In our discussions with content providers, all of them have indicated challenges in forecasting their longer-term demand requirements. A few aspects that influence growth rates include the following.

Maturing networks. The law of large numbers dictates that a large entity growing rapidly cannot maintain that pace of growth forever. We are certainly seeing evidence of this on major routes. This is a typical pattern for networks as they mature. Even with slowing cumulative growth rates, the incremental volume of bandwidth added each year is still massive. So, while global content provider bandwidth growth slowed to "only" 39% in 2021, this equates to an annual increase of 563 Tbps.

New applications. Artificial intelligence and virtual reality are most frequently cited as future applications that will drive demand. The degree to which these will impact international demand remains unclear.

Multiple product lines and users. Content providers' bandwidth demand comes from a large number of services within their companies. In the case of Google, there is search, YouTube, maps, cloud, and many more. It's also worth noting that the bandwidth demand for Google Cloud, AWS, and Microsoft Azure isn't related to these companies' internal demand, but rather on enterprises' implementation and usage of these cloud platforms.

Timing of new cables. In recent years, major content provider investments have reduced reliance on carriers, and have focused on securing enough wholly-owned fiber pairs to achieve sufficient route diversity. Increasingly, new capacity is added largely through the introduction of new cable systems. Thus, annual capacity growth rates observed on some routes could appear lumpy, as they are largely influenced by when new submarine cables enter service.

Supply Limitations

While the global shortage of chips is continuing to lead to some delays in network upgrades, these issues will likely be resolved within the next few years. However, other supply side factors could throttle the pace of demand growth in the longer term.

There is a limit to how many new submarine cables can be added each year.

There is a limit to how many new submarine cables can be added each year. Cable factories can only produce so many kilometers of cable a year, but there are also limited number of cable laying ships and experienced crews to engage in marine installation.

Increasing factory size, the number of installation vessels, and crews will certainly occur, but it takes several years for these measures to be implemented.

Geopolitical Concerns

While geopolitical concerns have always played a role in determining which companies deploy long-haul networks where, several recent developments are reshaping network deployment trends.

First of all, thawing relations between Israel and other Middle Eastern countries has allowed the potential for systems connecting Europe, the Middle East, and Asia to transit across Israel. Several planned projects, including the Blue and Raman cables, hope to capitalize on this opportunity.

In contrast, cable builders are finding it increasingly difficult to receive permits from China to deploy cables in the South China Sea. Operators of the planned Apricot cable hope to avoid this issue by building a cable from Japan to Singapore that runs to the east side of the Philippines.

In addition, U.S. government opposition to direct China-to-U.S. cables has boosted the development of several cables from Southeast Asia to the U.S., including Echo, Bifrost, and Hawaiki Nui.

Wholesale Market Challenges

The rapid expansion of major content providers’ networks has caused a shift in the global wholesale market.

Google, Microsoft, Meta (formerly Facebook), and Amazon are investing in new submarine cable systems and purchasing fiber pairs. This removes huge sources of demand from the addressable wholesale market. On the other hand, it drives scale to establish new submarine cable systems and lower overall unit costs.

Many submarine cable business models actually rely on this capital injection, allocating fiber and network shares to the largest consumers to cover initial investment costs, then selling remaining shares of system capacity as managed wholesale bandwidth.

Unit cost savings of large investments are a great incentive to investment for operators, but they don't want to be left with too much excess bandwidth. It's often a race to offload wholesale capacity before a new generation of lower-cost supply emerges.

Carriers most likely to succeed are those with massive internal demand and less dependence on wholesale market revenues.

Both content and carrier network operators are reckoning with massive bandwidth demand growth, driven by new applications and greater penetration into emerging markets.

Both content and carrier network operators are reckoning with massive bandwidth demand growth, driven by new applications and greater penetration into emerging markets. The sheer growth in supply will drive lower unit costs for bandwidth.

In the face of unrelenting price erosion, the challenge for wholesale operators is to carve out profitable niches where demand trumps competition.

Our Global Bandwidth Research Service assesses the state of the global telecom transport network industry and evaluates the factors that shape long-term demand growth and price erosion.

Download the 2022 Executive Summary to keep reading our latest analysis.

Jon Hjembo

Senior Research Manager Jonathan Hjembo joined TeleGeography in 2009 and heads the company’s data center research, tracking capacity development and pricing trends in key global markets. He also specializes in research on international transport and internet infrastructure development, with a particular focus on Eastern Europe, and he maintains the dataset for TeleGeography’s website, internetexchangemap.com.